March 30, 2021 – To build an understanding of the current market trends that are impacting the Memphis Metro area, the Chamber has been releasing monthly updates to our economic recovery.

To best gauge and position insights related to market activity, we are looking at the region through two lenses. The first is through the lens of traditional monthly indicators. These measures include the lower frequency jobs and unemployment figures and are often seen as lagging indicators of labor market activity. The second lens is through higher frequency weekly indicators. These measures include weekly unemployment insurance claims and job postings. Often, the higher frequency indicators are seen as leading indicators and can signal worsening or better employment outcomes for the region against the monthly reports.

With the release of the January 2021 unemployment numbers on March 19, these updates will provide a key snapshot of where the Memphis market sits as it relates to a recovery from the March/April 2020 contraction.

The Greater Memphis Chamber develops insights that help stakeholders ask the right questions to issues impacting our region’s economic competitiveness. To understand the impact of COVID in the current economic environment, the team analyzes data using a combination of sources such as the Bureau of Labor and Statistics as well as cutting-edge tools such as Burning Glass Labor Insights and EMSI, the Chamber aims to provide stakeholders with information that can help drive prosperity for all in the region.

{{cta(‘8b2652cc-425f-4fc2-91f3-d7cb450b6936’)}}

Indicators to Watch

Key insights from this report:

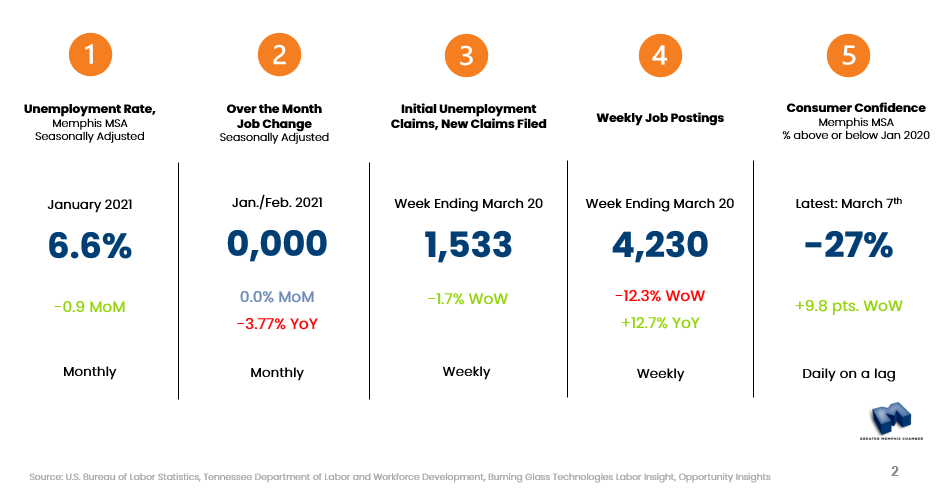

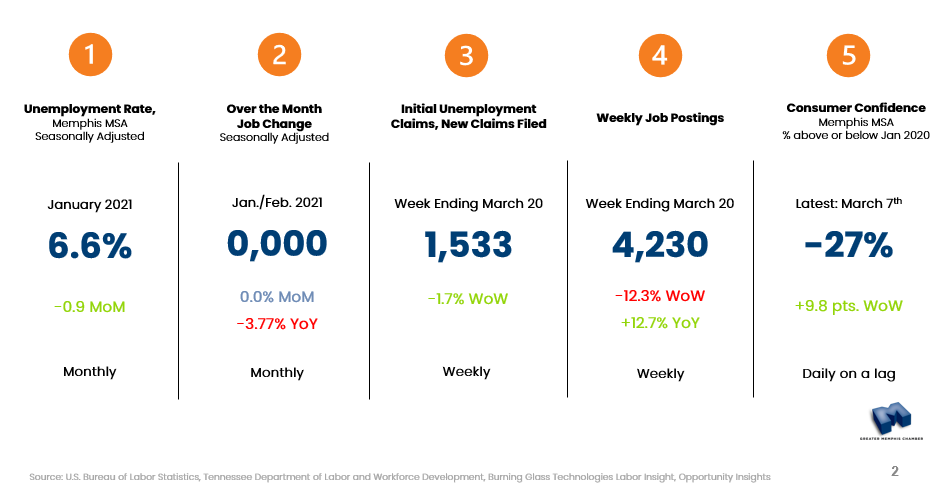

- Monthly Indicators, [lower frequency, lagging indicators]

- January 2021, the seasonally adjusted unemployment rate in the Greater Memphis MSA dropped 0.9 points to 6.6%. The decrease in the region’s unemployment rate is driven downward by a larger decline in its civilian labor force than its decline in employment. Meaning, more individuals exited the labor force than they did lose employment. This reduction thereby decreases the overall number of unemployed and tightens the gap between the civilian labor force and employed populations. The next release for (February 2021) metropolitan estimates will be April 7, 2021.

- Preliminary estimates of non-farm payrolls (jobs) in the Memphis metropolitan area neither increased nor decreased from January to February 2021. We anticipate adjustments as new data is published next month.

- Revisions to the 2020 jobs data shows a smaller magnitude of reduction paired with a slower rate of recovery. Initial estimates estimated a 73.1k job contraction, the revised 2021 estimates show a March/April contraction of 61.4k jobs.

- With the new estimates, the market has regained 64.5% of jobs lost March to April 2020. The region remains 3.3% below March 2020 and ranks well on recovery against a competitive set of metropolitan areas.

- Weekly Indicators, [higher frequency, leading indicators]

- After periods of lower initial claims activity – early January in Greater Memphis experienced sharp increases in initial claims. Those have since declined, falling 72% weeks ending Jan. 9th to March 20th.

- Online job postings, a proxy for employer demand have stabilized against historical levels. This is reassuring, as employers rebound and stabilize against new workplace dynamics. Week ending March 20, 2021 job postings were 12.7% higher than this same week in 2020.

- While the Greater Memphis market holds relatively high unemployment, many employers continue to hire. Broad based occupational groups are in demand in key areas including: Logistics and Supply Chain Support, Office Support and Customer Care, Healthcare, and Accommodation and Food Services.

- Consumer Spending, a proxy for consumer optimism, is the amount of money spent by households in an economy for durable and nondurable goods and services. Sharp decelerations are shown through the month of February and might be influenced by the large winter storm in February 2021. As of week-ending March 7, spending was -27% below January 2020.

{{cta(‘8b2652cc-425f-4fc2-91f3-d7cb450b6936’)}}

Questions? We would love to hear from you! Click here to send a question or request media access.

A New Day for Mobility in Memphis

Daily Updates | March 24, 2020