July 29, 2021 – To build an understanding of the current market trends that are impacting the Memphis Metro area, the Chamber has been releasing monthly updates to our economic recovery.

To best gauge and position insights related to market activity, we are looking at the region through two lenses. The first is through the lens of traditional monthly indicators. These measures include the lower frequency jobs and unemployment figures and are often seen as lagging indicators of labor market activity. The second lens is through higher frequency weekly indicators. These measures include weekly unemployment insurance claims and job postings. Often, the higher frequency indicators are seen as leading indicators and can signal worsening or better employment outcomes for the region against the monthly reports.

The Greater Memphis Chamber develops insights that help stakeholders ask the right questions to issues impacting our region’s economic competitiveness. To understand the impact of COVID in the current economic environment, the team analyzes data using a combination of sources such as the Bureau of Labor and Statistics as well as cutting-edge tools such as Burning Glass Labor Insights and EMSI, the Chamber aims to provide stakeholders with information that can help drive prosperity for all in the region.

{{cta(‘da7dfe26-76de-4828-8283-6e127c3014fc’)}}

Indicators to Watch

Key findings from this report:

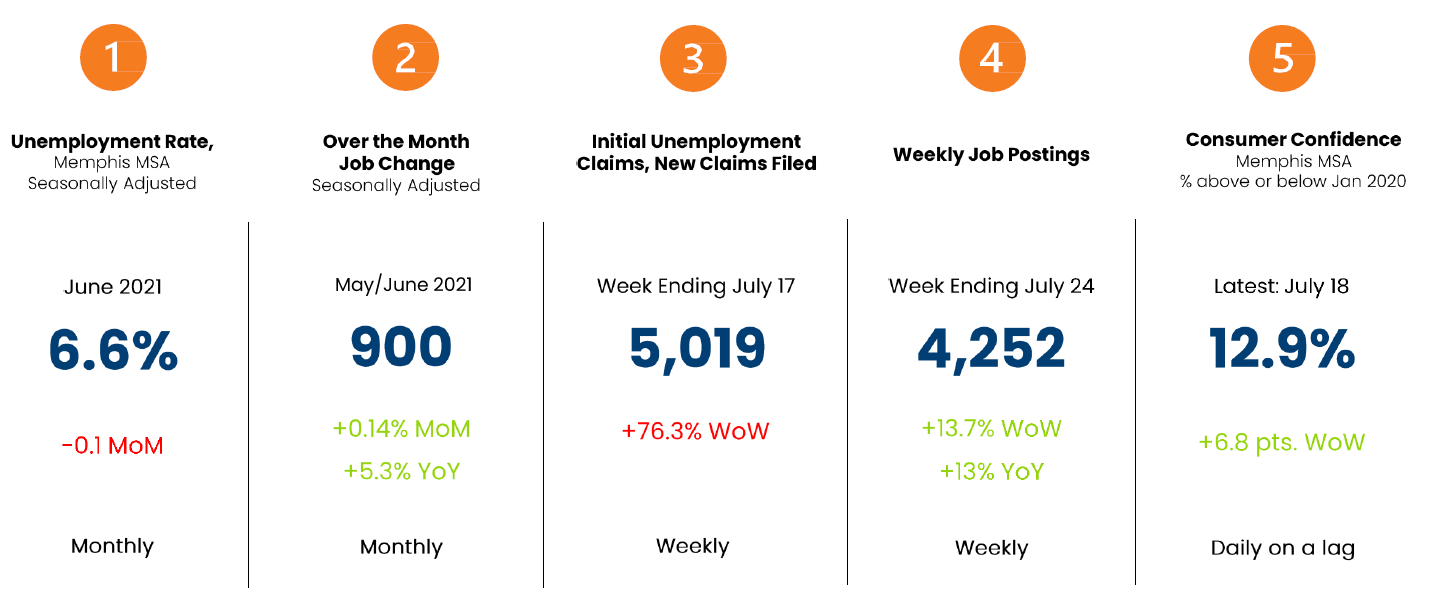

- Monthly Indicators, [lower frequency, lagging indicators]

-

- The Memphis region is 1.5% below its March 2020 level and ranks 1st on job recovery against a competitive set of metropolitan areas.

- June 2021, the seasonally adjusted unemployment rate in the Greater Memphis MSA was 6.6%, showing a consistent level from the past two months. The next release for (July 2021) metropolitan estimates will be September 1, 2021.

- Seasonally adjusted non-farm payrolls (jobs) in the Memphis metropolitan area increased by 900 (0.14%) from May to June 2021.

- The industry of Professional/Business Services is 10.8% above its March 2020 level. Construction, Transportation, and Manufacturing all show some level of growth from their respective March 2020 level.

- Weekly Indicators, [higher frequency, leading indicators]

- After falling initial through May and June 2021, initial claims have increased over 300% from week ending July 7th to week ending July 17th.

- While job postings saw an increase by over 100% in the Q1 2021 and half of Q2 2021, postings have seen a small contraction while still maintaining averages well above those of the past three years.

- While the Greater Memphis market holds moderately high unemployment, many employers continue to hire. Broad based occupational groups are in demand in key areas including Warehousing, Truck Driving, Nursing, and Retail positions.

- Consumer Spending, a proxy for consumer optimism, is the amount of money spent by households in an economy for durable and nondurable goods and services. Sharp declines are shown through the month of February and might be influenced by the large winter storm in February 2021. As of June 13th, spending was 6.1% above January 2020.

- Adding positive pressure to jobs growth, consumer spending within key categories of Restaurants and Hotels, as well as Entertainment and Recreation are up 6% and 1.9%, respectively.

{{cta(‘da7dfe26-76de-4828-8283-6e127c3014fc’)}}

Questions? We would love to hear from you! Click here to send a question or request media access.

Meet the Chairman’s Circle: Sarah Jemison